Printable PDF version

Subscribe to our newsletter

Lean but not Mean

Big Data in Construction

Prediction Problems

Construction

Management Specialists

111 Pine Street, Suite 1315

San Francisco, CA 94111

(415) 981-9430 (San Francisco office)

6518 Lonetree Blvd., Suite 164

Rocklin, CA 95765

(916) 742-1770 (Sacramento office)

600 B Street

San Diego, CA 92101

(619) 814-6793 (San Diego office)

8538 173rd Avenue NE

Redmond, WA 98052

(206) 571-0128 (Seattle office)

2063 Grant Road

Los Altos, CA 94024

(650) 386-1728 (South Bay office)

7083 Hollywood Blvd., 4th Floor

Los Angeles, CA 90028

(424) 343-2652 (Los Angeles, CA office)

1a Zoe House, Church Road, Greystones

Wicklow, A63 WK40, Ireland

+353 86-600-1352 (Europe office)

www.TBDconsultants.com

Lean Construction is becoming a popular term, but different companies may be implementing it in different ways. In this article we look at at what it is that makes construction Lean.

This era could be called the Data Age. Here we look at what Big Data is, and how it is changing the construction process.

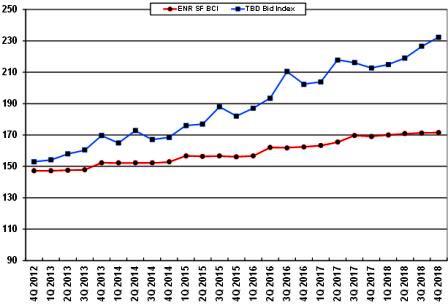

The stock markets dont seem to know which way they want to move, with the result that businesses are becoming concerned about the possibility of a recession. As a consequence, we saw US construction-starts dropping by 10% in December 2018, mostly due to the non-residential sector, although starts finished the year marginally up from 2017. The AIAs Architectural Billings Index had also been dropping at the end of 2018, but has been showing a strengthening again at the beginning of 2019, with all regions of the country showing positive growth in design work which should lead to more on-site construction.

The tariff war has been one concern for markets, but at time of writing (early March) it is looking as though some form of agreement between the US and China is coming, and that should result in a reduction or removal of many tariffs. The tariffs were designed to help improve the trade gap that the US has with the rest of the world, but the trade deficit actually increased substantially in 2018 over 2017. Such increase might not be totally dependent on the tariff war. Despite a number of concerns, business in the US has been flourishing quite well, consumer confidence has remained high, and the US GDP growth rate has been continuing to follow an upward trend. Meanwhile, Europe has been showing fairly stagnant growth and China has admitted that its growth rate has been dropping. How accurate the official China growth rates are remains questionable, but, although it has been dropping, it remains impressive. The growing market here in the US means we should be buying more, while if elsewhere growth is stunted, they wont be buying as much, so the trade deficit can expect to be hit. The question is, how much of the slowdown elsewhere is due to the tariff war or to other factors.

The Feds interest rate increases has been another concern, although the fact that it felt it could make those increases shows that it sees the economy as strong. Rates are still at historic lows, especially considering the fact that businesses are doing well. The low levels of inflation (and we are not talking about construction cost increases here) does mean that there is little pressure on the Fed to push interest rates much higher. However, having such low rates also means that they will have weaker tools available if and when we do enter another recession and the economy needs a boost.

The bull market has just passed its tenth anniversary, which is an exceptional run when looking at recent cycles that indicate recessions happen around every nine years. But we know that there is nothing fixed about these cycles, or anything necessarily logical about the markets which are mainly driven by fear and greed. It is inevitable that another recession will come, although the next one is likely to be mild compared to the previous, and currently there is little indication that one is coming soon. Job growth remains good (despite the dip in February) and consumer spending is high, so, although there are plenty of potential problems out there, the economy seems happy to shrug them off for now.

Geoff Canham, Editor, TBD San Francisco

Design consultant: Katie Levine of Vallance, Inc.